Navigating Tax Seasons: A Donor’s Guide to 80G in 2025

Your financial management is incomplete without tax planning. A lot of people choose donations to make a social impact, a move that also brings a welcome donation rebate in income tax. The government in India encourages this charity with tax incentives. The most powerful one is the deduction under Section 80G of Income Tax Act. But now the new income tax regime is the default option, raising a huge question for the 2025-2026 financial year. Which path is better for people who donate to causes they care about?

This guide breaks down section 80G of the Income Tax Act. We will compare the old and new tax regimes so you can make a smart, confident choice. Remember, every person’s financial situation is different. The only way to get the best outcome is to carefully evaluate your options.

The Power of Section 80G

By utilising this provision, Section 80G of the Income Tax Act, you can achieve substantial tax savings. It gives you a tax deduction for any eligible donations you make. Your taxable income goes down by a percentage of the amount you donated.

This is the government’s method for rewarding citizens who help develop society. However, there’s one catch: to get the benefit, your money must go to a charitable institution with a valid 80G Income Tax Exemption registration. The exact deduction amount varies. Some organisations qualify you for a 100% deduction, while others offer 50%. This provision can really move the needle, letting you support important work while actively managing your tax bill.

Old Tax Regime: The Deduction and Exemption Route

The old tax regime operates on a model that revolves around deductions and exemptions. These are the tools used to calculate your final taxable income. You have the freedom to claim a wide variety of deductions for investments and expenses, including your life insurance premiums, contributions to a provident fund, and the interest on your home loan.

The most common deductions fall under a few key sections.

- Section 80C: It handles investments and costs like the Employees’ Provident Fund (EPF), Public Provident Fund (PPF), life insurance, and your children’s tuition fees, with a maximum deduction of ₹1,50,000.

- Section 80D: Health insurance premiums for you, your family, and your parents are deductible under this.

- Section 24(b): You can claim a deduction for the interest paid on your home loan by utilising this section.

The old regime’s structure makes the 80G Income Tax Exemption an essential provision for taxpayers who wish to donate. Your donation to a registered NGO, such as Bal Raksha Bharat (also known as Save the Children India), allows you to claim up to a maximum of 50% or 100% deduction. That deduction hits your gross total income directly. The result is a smaller overall tax burden. If you make big investments in tax-saving instruments, the old regime is a very strong choice. It is a system built to reward saving and investing for your future.

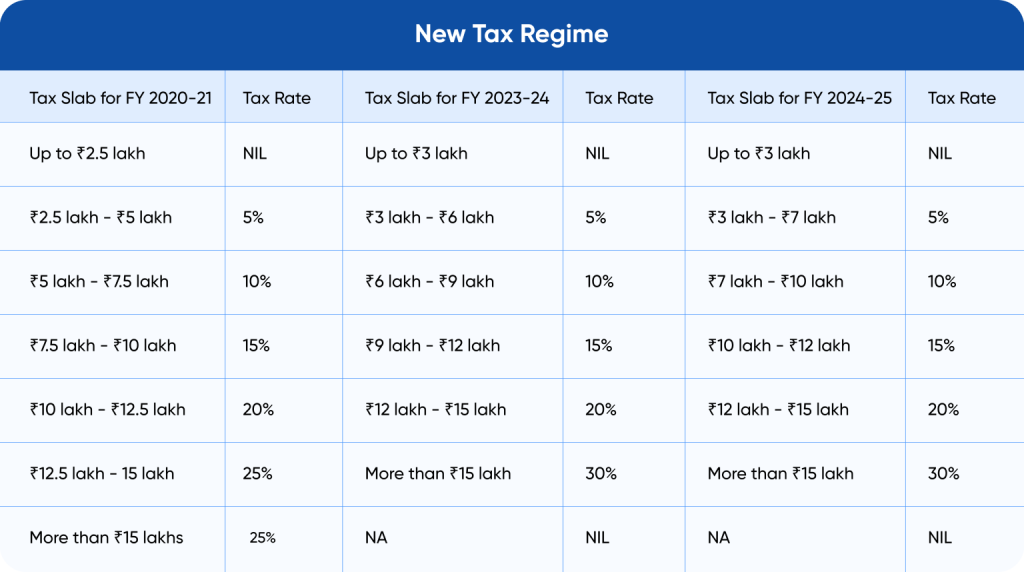

New Tax Regime: Lower Rates, Simpler System

The new regime, which is now the default, is structured differently. It provides lower income tax exemption slab rates. The trade-off is that it removes nearly every deduction and exemption. The government’s goal was a simpler, more direct system, especially for people who do not have a portfolio of qualifying investments or expenses.

This system is defined by a few core traits.

- Lower Tax Slabs: Your tax rates are reduced across different income brackets when you compare them to the old regime.

- Minimal Exemptions: It gets rid of most major deductions, including everything under Section 80C, 80D, and the standard deduction.

- No 80G Benefit: Here is the most important part for philanthropists. Section 80G of Income Tax Act benefit does not exist here.

This is a critical difference you must weigh. The new regime provides a lower tax rate up front, but it is the wrong option if you rely on deductions to lower your taxes. The focus is purely on a reduced tax rate.

Which Path Is For You?

There is no simple answer here. The selection is subjective and solely based on your financial habits and your long-term objectives. A deep dive into your own finances for the 2025-2026 financial year is the only way forward.

When to Choose the Old Regime

The old regime is the right fit if you are a disciplined investor.

- It makes sense if you have large investments that qualify for deductions under sections like 80C.

- You should lean this way if you have a home loan interest deduction or pay for health insurance.

- Most importantly, if you plan to make a charitable donation and want the 80G Income Tax Exemption, the old regime is your only choice.

- All these deductions combined can drop you into a much lower tax bracket.

When to Choose the New Regime

You might find the new tax regime is a better fit in other cases.

- Consider it if you are early in your financial journey and do not have many tax-saving investments.

- If your income falls into the lower brackets, the lower rates might give you a better outcome.

- Those who do not want to track documentation in a complex system of calculations also choose a new regime.

- You are not concerned with claiming deductions.

The appeal is its simplicity and the higher take-home pay from day one. It is highly recommended to use a tax calculator. Put in your numbers and compare the tax liability under both regimes. That will give you a clear, precise picture. It is also prudent to speak to a financial advisor.

The Impact of Philanthropy

Leaving aside the tax regimes, giving is a very strong force. The donation rebate in income tax is a great perk, but the true value comes from giving a child a better future. Many non-governmental organisations work tirelessly to create a more nurturing environment for children by focusing on key areas. For instance, Bal Raksha Bharat is a respected organisation dedicated to ensuring every child in India gets a healthy start, an opportunity to learn, and is protected from harm.

These non-profits are crucial in society, as their work covers all aspects of a child’s development:

- Providing healthcare: They ensure children have access to essential medical care and proper nutrition.

- Ensuring access to quality education: They help build the foundation for a strong future.

- Offering humanitarian aid during emergencies: They act as a beacon of hope in a crisis.

When you support a trusted organisation that champions the welfare of children, you contribute directly to creating a safer and more nurturing country for all.

Final Words

Your decision boils down to a hard look at your financial habits. The old regime is a powerful tool for savers and planners, offering the 80G Income Tax Exemption along with many other deductions.

The new regime is a simplified structure with lower tax rates, best suited for those who do not have many deductions to claim. Whether for your own finances or for the most vulnerable in society, the goal is always a better future. Understanding Section 80G of the Income Tax Act helps you make a choice that is both financially intelligent and socially powerful.

| Make a difference with your donation! Empower the community and unlock your income tax exemption, turning your compassion into a tangible financial benefit. |

FAQs

- Is the deduction under Section 80G available in both old and new tax regimes?

No. You only get the Section 80G deduction in the old tax regime. This is a critical difference between the two systems.

- How much deduction can a person claim for a donation rebate in income tax under Section 80G?

The deduction amount from the 80G Income Tax Exemption depends entirely on the receiving organisation. It is either 100% or 50% of what you donated, sometimes with a qualifying limit.

- What is the difference between Section 80C and Section 80G?

Section 80C covers deductions for specific investments you make, like life insurance, provident funds, or tuition fees. Section 80G of Income Tax Act is completely different. It provides a donation rebate for your contributions to approved charities and relief funds.

- What documents are required to claim the deduction under Section 80G?

You must get a valid receipt for the charitable donations. This receipt has to show the organisation’s name, address, and PAN, as well as your name and the amount you donated. It must also clearly state the organisation’s registration number under Section 80G.